The Euro as a Carry Trade Funder ... Surprising?

Nothing is so bad, that it isn't good for something

So goes an old adage in my home country (and I would imagine elsewhere too) and perhaps if hard burdened Eurozone policy makers and investors are finding it hard to find any kind of (positive) silver lining in the current debacle, they may just want to remember that old of oldest saying. I am of course talking about the Euro here and while its recent fall from grace has been linked to all kinds of nastiness in the form of a Eurozone break-up/collapse as well as the final nail in the coffin of those who once argued that the Euro would surpass the USD as the global reserve currency [1], it is also going to act as a much needed leg of support to those economies most in need of export performance in the absense of domestic demand. As the tally of the financial crisis increases and as the demographic transition soldiers on this is fast becoming all the Eurozone economies combined [2] (click for better viewing).

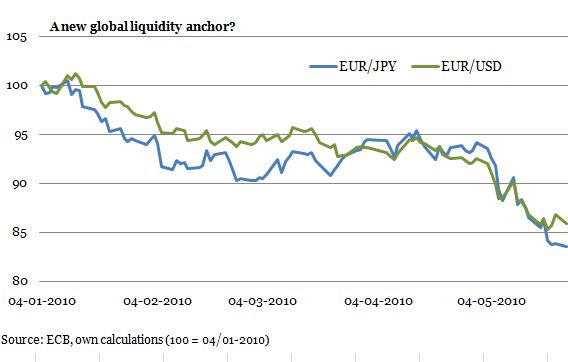

Since the beginning of 2010 the Euro has depreciated 14% and 16.5% agains the USD and JPY respectively and this is remarkable in an environment where risk aversion has unwound. In short; when it comes to the game of cards in terms of global liquidity/capital flows where holding old maid means that you buy bear the brunt of intra-G3 appreciation. This is what I wrote in my sneek-peek into 2010 G3 FX markets;

In an G3 context, 2010 clearly holds the potential for Dollar strength, but timing and intensity is going to differ. Most major research houses see the USD/JPY as a strong candidate for a correction that could move the pair back in the 100s. I concur. Whatever speed the US economy will have in 2010, Japan will be the laggard and the BOJ will be dragged kicking and screaming into a full out battery of QE measures.

Buy the Old Maid. If the rally in risky assets continue into 2010 and beyond, the Euro will be holding the Old Maid amongst the G3. If the recovery is stopped in its tracks it is very likely that it will be from an event conjured in Europe making the USD holder of Old Maid. The former looks the most plausible scenario at this point in time with the notable qualifier that the USD should strenghten against the JPY. In this way, the Old Maid will shift hands from the JPY to the Euro and potentially the USD with the outlook for the EUR/USD not easy to call.

In my book the EUR/USD looks way too high even in the 1.40s. However, we have seen before that this pair may continue to rally so it is worth treating this one with care. Societe Générale sees dollar weakness sustained (except versus the JPY) well into 2010 and thus the EUR/USD continuing to drift upwards. I only conditionally agree. Especially I would emphasize the fact that the risks to the Euro, by far, out match those to the USD at the current juncture. In this way, I am less sanguine when it comes to the continuation of the ”recovery” and thus the rally in risky assets.

I will let my readers judge the accuracy of my argument but I don't think it is too far off the mark. Consequently, I was not particularly suprised by this piece today running across the Bloomberg wire that FX punters and other of their ilk are beginning to look to the Euro as a source of global liquidity to play the carry wheel in high yield economies.

(quote Bloomberg)

The fastest convergence in short-term interest rates in almost a year is making the euro a surprise addition to currencies used to finance investments in higher- yielding assets. “The hot guys are moving into using the euro as a funding currency,” said John Taylor, who helps oversee $7.5 billion as chairman of New York-based FX Concepts LLC, manager of the world’s largest foreign-exchange hedge fund. “It’s not quite as cheap as the yen but it’s a lot safer in a crisis, because the worse the world looks the worse the euro looks.”

Borrowing in euros to finance an investment in the Australian dollar, New Zealand dollar, Brazilian real and Norwegian krone returned 10 percent in the past 6 months, according to data compiled by Bloomberg. The same trade using the dollar instead of the 16-nation currency resulted in a 7.5 percent loss, and a 7.4 percent decline with the yen. Deteriorating economic prospects in the euro area have helped push down the cost of short-term borrowing in Europe relative to the U.S. The London interbank offered rate, or Libor, for three-month loans in euros fell to within about 14 basis points, or 0.14 percentage point, of the dollar rate on May 21, from 26 basis points at the end of April and 40 on Dec. 31, according to data from the British Bankers’ Association.

Libor for loans in dollars for three months was 0.497 percent at the end of last week, compared with 0.636 percent for euros, the BBA said. The European Central Bank’s main refinancing rate is 1 percent, while the Federal Reserve’s target rate for overnight loans is as low as zero.

Now, I am sure that the Eurocrats would rather have the Euro gunning for reserve status and certainly this goes for the ECB hawks who have so far, and decisively in the context of the initiation of QE, been drowned in a sea of dove feathers. However, being a carry trade funder has its advantages too; just ask Japan who has benefitted from this role a long time up until of course the Fed rushed into QE on the back of the financial crisis as well as it appears that Japan's own horrible growth and debt outlook has taken the, temporary, backseat to the crisis in Europe. As Andreas Hahner, a money manager at Allianz Global Investors, is quoted by Bloomberg; you need three things to be a carry trade funder. Low interest rates(check!), depreciation/relative weakness (check) and low volatility (well, check for now). However, Mr. Hahner is right to point to the fact that the bounce back in the Euro could flush out many a European version of Ms Watanabe.

But then again, which boounce back would he be talking about here?

Certainly, in relation to the G3 the big problem is that the long term growth prospect for the US looks decidedly brighter than for Europe and Japan (demographics remember) and this is a "problem" since we were also supposed to correct those blasted imbalances. In fact, one cannot help but feel that if Germany really wants wealth preservation and vigilance against inflation, let them have it, but they need to know what it means. I would consequently submit that in terms of keeping the Eurozone in one piece and in its current form will require a sea-change at the ECB. We have seen the first steps to this with the intiation of QE, but what markets have not faced up to yet is the duration of this policy measure. It won't just go away folks; it is here to say. Whether it also means that the Euro is now to become a carry trade funder of choice is a significant question since if this is the case, it means that it will also begin to trade like one. I for one would not be surprised to see this and investors should take note of the change in discourse on the Euro here [3].

---

[1] - About time too; some of us has argued this for the better part of the last 3 years!

[2] - In this sense, there IS convergence which is actually an interesting point to ponder in terms of general reflection.

[3] - Well, of course, you should not take note of me not being surprised :)