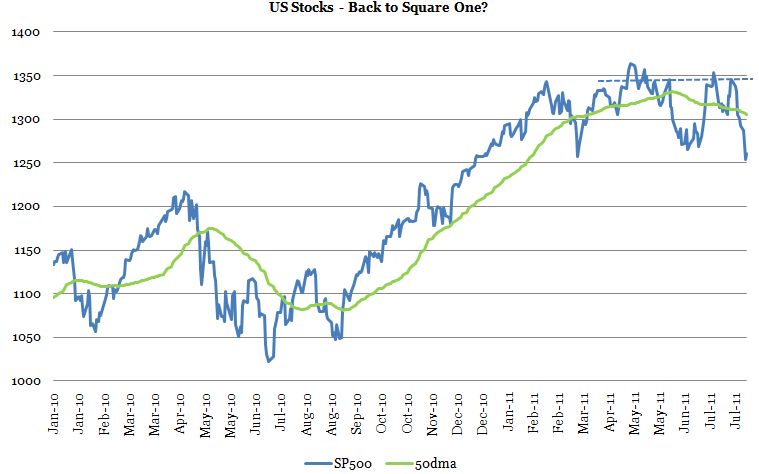

Random Shots - All Back to Square One?

Starting a new job and settling in a new city/flat has proved a little more unsettling for my blogging efforts than I had expected. Anyway, what better time to return to the fray when the SP500 completes its worst run in a long time returning to levels not last seen since March where we thought we had to write off the entire Japanese economy as a nuclear wasteland. So, is it all back to square one for the already weak recovery?

Arguably though the catalyst this time is more sinister in that it cannot really be pinned on any single event. Surely, the debt ceiling charade and the prospects of Spain and Italy spiralling further into the arms of what ever bailout that might be on offer are catalysts in themselves, but the underlying economic data is getting increasingly sour.

All the leading data we are looking at, both in terms of the global breadth of economic momentum and specifically on the US economy have rolled over in a dangerous fashion and a recession in the US cannot be entirely ruled out. Indeed, on some measures we would even be calling one. Elsewhere, the slump in the July Australian PMI also suggests that one of the hitherto strongest economies in the global recovery may be about to embark on its own homegrown downturn.

It was also interesting to see the SNB finally cave in (yet again) to the relentless rise of the CHF despite the bank's efforts both communicative and with hard money to starve off the beast. As I have remarked before, safe haven flows hurts and can be akin to holding Old Maid. Indeed, it may turn interest rate decisions on their head as rates will be lowered going into a melt up of economic activity to attempt to deter speculative inflows.

Generally, one of the most obvious consequences of the recent bout of weakness will be that more stimulus is in the pipeline, at least in the US economy whereas the ECB will probably need a little time before the reality dawns on them. However, the underlying inflection point between an economic recovery that is clearly turning out much weaker than expected and the reality of too much debt is starting to hurt. In that vein, it is difficult to see a viable way out of the obvious need to cut spending and reign in excessive public spending with the simple fact that what has largely driven GDP in the recovery has been government consumption and investment.

We can consequently expect that the Krugmans of the world to get another big chunk of the discourse as the call for further and bolder stimulus packages increases. In this respect, the Squid had nice note out on Monday on the possible avenues a new round of QE would take where the main message seems to be that the Fed will try to further cement its position of low rates for an extended period. But more interestingly is the widespread expectation that if the Fed engages in further asset purchases it will be on the long end of treasury curve and thus to flatten the curve on the long end. Surely, this makes sense in so far as goes the idea that the housing market remains in an extremely poor condition. Mortgage rates are thus likely to be driven more by long term rates than rates on the short end or at the middle. Coupled with outright targeted asset purchases of MBS using the proceeds from its securities portfolio the Fed would be signalling that the size of its balance sheet will remain inact.

Sufficient on to the day and all that but with the current sinister backdrop of market currents and poor economic data we can expect Bernanke to step up any time now.

It has occured to me here that what we might be facing in the developed world is a mirror image of the situation in the emerging world and that the combination is not the best of mixtures for the global economy.

Consider then the situation e.g. in India where the RBI is trying frantically to weigh against excessive government spending not to mention China where you get the distinct feeling that at least some part of the inflation problem comes from the central authorities' credit policies (or lack of tight standards). Conversely, in the developed world austerity is the name of the game quite simply out of necessity and faced with extremely fragile economies it is largely up to the central banks to attempt giving the economy some tailwind. On a personal note, this is also why I consider the ECB's recent hiking campaign as the biggest policy failure since, well, they raised just before a recession the last time. The very best we can hope for in Europe is then not a recovery but simply that we might end up back at square one.