Random Shots - Down, Up or Sideways?

Of all the permutations of growth stories, scares and soft patches investors should remember that when all is said and done, the economy and market can only do three things; move down, up or sideways. Of the three, the last state is often the most interesting and challenging since while in such a state the debate will be centered on two main themes. Firstly, the reasons for said sideways movement that broke and otherwise upward or downward trend and secondly whether the market and economy will eventually will break this sideways movement by launching a new or resuming the old trend.

Of all the permutations of growth stories, scares and soft patches investors should remember that when all is said and done, the economy and market can only do three things; move down, up or sideways. Of the three, the last state is often the most interesting and challenging since while in such a state the debate will be centered on two main themes. Firstly, the reasons for said sideways movement that broke and otherwise upward or downward trend and secondly whether the market and economy will eventually will break this sideways movement by launching a new or resuming the old trend.

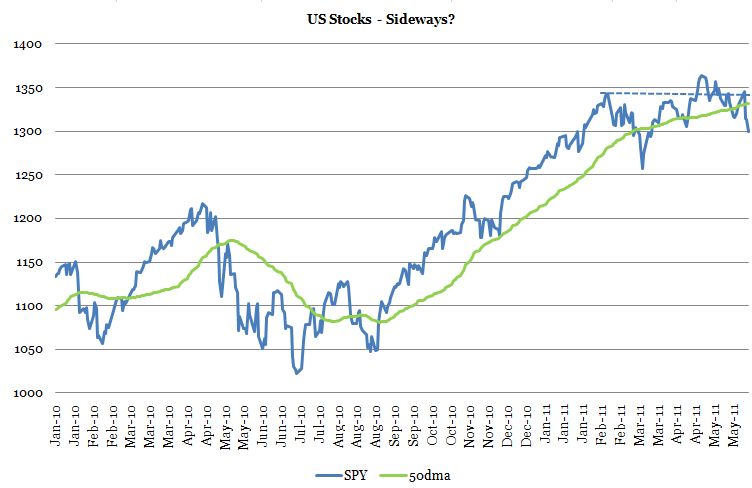

As far as goes the market's erratic movement in the first half of 2011 the immediate reason for the abrupt halt to the positive trend was the devastation of the earthquake in Japan and the subsequent (short term) slump of global equity markets. While the SP500 did have a sniff at new highs at the end of April and into May this level could not be held and we have since poodled back down below support levels.

One of the problems in the current environment is that while the immediate macroeconomic outlook is one of a slowdown, the question of whether it will turn into a more lasting double dip is more difficult to determine.

(click on charts for better viewing)

On the face of it, we should now be approaching the point at which the global economy reveals to us just what level of growth that we can expect to be "normal" and crucially; where this growth is supposed to come from.

What might be starting to creep up on investors' screen is that the answer to the question above might not be what they anticipated.

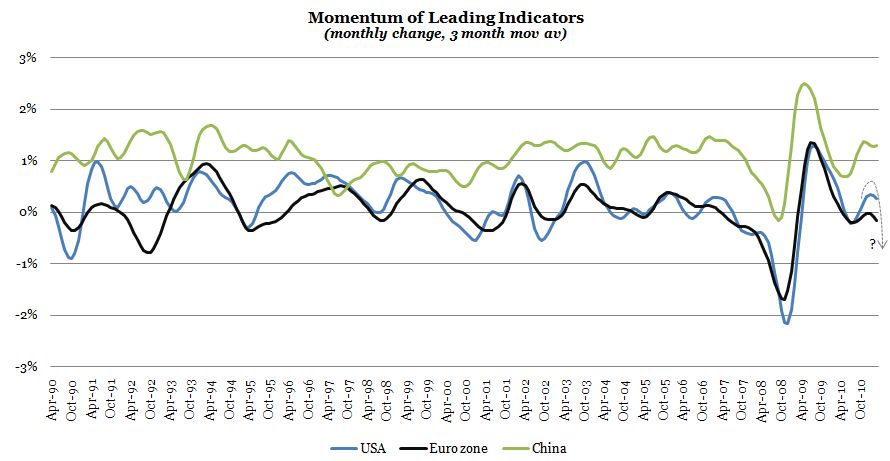

On the basis of the data I am looking at, the upward momentum of global leading indicators peaked a year ago (in Q4-09) and momentum has since steadily declined to reflect growth returning to "normal" after the sharp recovery following the global financial crisis. The most recent soft patch in the middle of 2010 gave way to a rebound, but the key is whether the recent relative decline in growth momentum is a messenger of a more sustained downturn or simply another so-called mid cycle soft patch. OECD's leading indicators point to a definite slowdown but also to a rebound towards the end of the year. The main point really is one of divergence between economies.

In Europe it has become almost unbearably painful to watch the charade which surrounds the slowmotion default in Greece and the frantic attempts by policy makers to suggest that all is well and the next loan tranche is coming. Everyone can understand why politicians, of all people, should not give way to short term panic and whims of the market but we are way past the point of no return and we need a credible long term solution to not only Greece but indeed the debt overhang in the entire so-called periphery.

Not surprisingly, the macroeconomic backdrop of the ongoing fiddling while Rome (or was that Athens or Madrid?) burns is deteriorating. Morgan Stanley recently noted then that;

We see increasing evidence that the euro area business cycle has reached a turning-point. This verdict comes very clearly from our Surprise Gap Index, which plunged deep into negative territory in May. Our Surprise Gap Index is our long-standing favourite proprietary indicator to pick out the turning points in the euro area business cycle.

My only quibble would be that some economies in the Eurozone never experienced an upturn in the first place. It must now be clear for everyone that choosing to put faith entirely in a process of internal devaluation with little or no additional help from the ECB (and even interest rate hikes to boot) has put us in a situation which is far more dangerous than the one we set off from.

A sovereign default was always going to be costly and the main channel of transmission to the real economy will the capital shortfall at banks and who essentially should pay to recapitalise them. Yet, the continuing steadfast position that any form of restructuring is out of the question pushed us further towards the point where events overtake policy makers to such an extent as to foster a collapse of sentiment and trust which will ricochet far beyond the growing queues in front of Athens' banks.

In emerging markets, growth will remain strong but policy makers in key countries such as India and China have grown weary over inflation and especially in the former seems to be content on accepting short and perhaps even medium term slowdowns in order to tackle inflation. There is no risk of a recession in emerging markets (and thus the global economy) at this point but any slowdown in emerging markets will be an important litmus test for the developed world and thus just how dependent we may now be on a continuing expansion in the so-called developing world.

Even in the face of mounting inflation problems as a result of importing low interest rates from the US I remain constructive on emerging markets and especially on China. Quite simply, I am working under the assumption that while authorities may move clamp down on inflation and excess growth in credit the main bias is thoroughly towards letting the boom continue. If I see signs that this assumption may be wrong I will duly change my views, but so far so good.

But the real issue which may decide whether sideways movement in growth and market returns gives way to continued upside or renewed downside is what happens in the US and specifically, whether the Fed is readying a new round of QE3.

Priming the Pumps for a New Round of QE?

Bernanke is famously on record for linking success of QE to the ongoing strength in the stock market and while I have myself given support to this notion on the basis of simple empirical fact that the wealth effect seems to be increasing over time, it is the effect on the real economy we should rather be focusing on. John P. Hussman recently posed the following simple question;

My intent is not to argue strongly that the economy cannot continue to expand as fiscal and monetary stimulus comes off, but instead to at least ask why this should be expected as a foregone conclusion. On the basis of leading indices of economic activity, we observe more indications of economic slowing worldwide than we observe growth. Moreover, strong periods of employment growth have historically been preceded by high, not low, real interest rates. This is far from a perfect relationship, but it is clear that historically, high real interest rates are far more indicative of strong demand for credit, new investment, and new employment than low real interest rates are.

We will never know what kind of independent momentum the economy in the US (or elsewhere) is able to maintain without actually pulling back stimulus, but the question is whether now is the time to take the chance.

The question of further QE would seem to currently be a mute point. Almost all analysts I have been reading and the general message droning in off the wires of Bloomberg and CNBC is that QE3 won't happen. Recently, I watched a small clip in which chief economist at Goldman O'Neill simply noted that there wouldn't be QE3 because there was no need for it. In a recent post at his new blog my friend Edward Hugh also parses the entrails of the potentials of QE3 and while some analysts are beginning to pencil in the prospects of another round of QE it seems that it is a much more difficult call this time around.

For example he quotes a recent analysis by BNP Paribas;

“With equities, credit and commodities all continuing to trade in a range disconnected from weaker economic realities being transmitted via surveys, hard data and the interest rate markets, we arrive at the same conclusion as we have over the last month, primarily that financial assets are fully expecting further quantitative easing if the need arises”.

This would seem to be reasonable conclusion and essentially stipulates how the break down of any sideways trend would be contingent on whether the Fed decided to provide a further dose of QE. However, I reiterate that the general sentiment I get is that the current slowdown is different and that no further QE is needed. A lot here obviously depends on how believe inflation and inflation expectations to evolve. Edward quotes analysts noting that since the labour market is improving, core inflation edging up as well as inflation expectations taking off from sub-zero deflation territory QE3 is not needed. Yet, as I say, none of this is clear cut. Here is Edward;

Really I don’t buy these latter two arguments, and I don’t buy them for a number of reasons (I am not sure inflation expectations won’t be coming down, indeed I don’t see why they shouldn’t), but number one among them would be the danger of “event risk” in Europe. Basically it is important to understand the global mechanisms that are at work here, and the global implications of local decisions. If the global economy has been growing reasonably well over the last six months it is because what Nouriel Roubini once called a “wall of liquidity” is seeping out of the United States, where solvent domestic demand for credit is flat and will remain flat due to the private indebtedness problem (remember US “over consumption” (the high proportion of GDP which has been consumption driven) has only been the mirror image of Chinese “over investment” and we that live in a world which badly needs to rebalance).

This argument is interesting to consider in itself in the sense that it suggests how the mechanism by which carry trade flows funded in USD has been the main source of the incipient global recovery. The flipside to this argument obviously is that the continuing ultra loose liquidity adds considerable volatility to commodity prices which, in itself, is detrimental to growth. In addition, strong surges of headline inflation may also lead to stagflation which is evident e.g. in the UK.

The main issue however is that that the data in the US is turning sour and the housing market has not yet made it to the party. This week's job report was poor and, apart from an improving trade deficit, a faint hue of gloominess is returning to the US economy. But, are we looking at a real recession risk? The data I am looking at and the, after all, still positive momentum of leading indicators suggests no and I am moving in behind a general consensus. Hussman synthesizes the main position in his latest column;

In recent weeks, and particularly in last week's ISM, employment claims and unemployment reports, we've observed a substantial weakening in measures of economic growth. At present, the evidence of economic deterioration is not severe - as I noted in 2000, 2007 and last summer, recession evidence is best obtained from a syndrome of conditions, including the behavior of the yield curve, credit spreads, stock prices, production, and employment growth. While all of these components have weakened, they have not deteriorated to the extent that has (always) accompanied the onset of recessions.

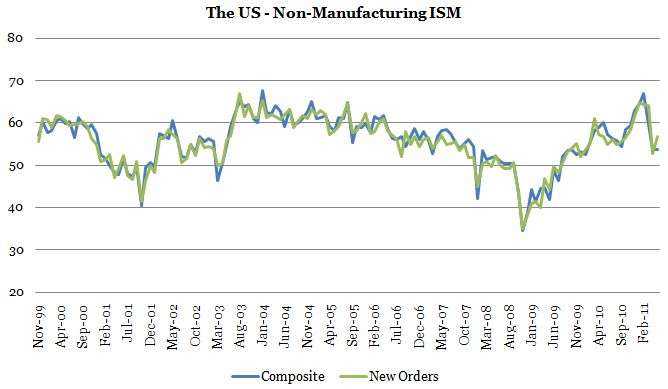

So far, so good then. I would reiterate the point on the ISM indices which have turned decisively down lately with especially the manufacturing ISM shifting down considerably both in terms of the coincident activity index and new orders. The same goes for the non-manufacturing ISM although it eeked out a bright spot in May with an increase in the new orders component.

The latest from Morgan Stanley's Gerald Minack also suggests that we should be sanguine on the US economy going into the second half of 2011 even if he merely postpones the deflation/growth scare 6 months.

Investors again are worried about the expansion faltering. However, better second-half growth data – notably, in the U.S. – should help risk assets, particularly DM equities. The 2012 outlook remains problematic, however, with growth set to slow in most major blocs, bar the special case of Japan.

All this then seems to indicate that while the Fed certainly will be committed to low interest rates it might be more difficult for investors to genuinely expect a new round of full fledged QE3. This should also be seen in the context of the ongoing debate of whether QE works at all and whether the associated volatility in commodity prices is worth it. In his recent column Hussman puts his thumbs down;

Rather, the policy [QE] has failed because it focused on easing constraints (bank reserves, short-term interest rates) that weren't binding in the first place. Very simply, neither the Fed's policy, nor the fiscal policy initiatives to date, address the central challenge that the U.S. economy faces, which is the debt burden on households.

This raises the central question of just what policy tools that should be applied in the context of a (global) balance sheet recession baring the case in which one simply lets the economy spiral into debt deflation and eventual widespread private and sovereign defaults. One obvious solution would be give some form of debt relief on a national scale and then let Fed re-capitalise the financial sector through equity or debt purchases, but just how much would be needed and what would this imply in terms of the Fed becoming an owner of capital rather than a custodian of the Greenback and its value. Besides, this solution has been tried in Ireland where it was merely the government who assumed a guarantee of its bad banks only then to have neatly forgotten the fact that monetary policy (and thus the ability to actually hone up to the guarantee through issuance of liabilities (i.e. currency)) had been ceded to Frankfurt a long time ago. The US naturally would be in a different situation but it would require the Fed to drastically shifts its QE towards private sector securities rather than government bonds.

James Hamilton is also lukewarm regarding the end of QE2 for the same reasons as Hussman. The basic message is that QE2 has only had a modest effect, but also more importantly that the Fed can not be expected to exert much of an effect in the first place. While this may be true Hamilton does point us towards one key point which relates to the fact that although the Fed might not actually be starting off a new round of Treasury purchases, this does not mean that the Fed's balance sheet will actually shrink.

A more technical issue then is another hotly debated question in relation to who the marginal buyer of treasury bonds will be once the Fed steps back from the fray. The interesting thing about the effect of QE is that while one would expect QE to help keep a lid on yields, the opposite has actually occured as e.g. QE2 has led to an increase in yields (which now looks about to reverse) on the back of the improving economic outlook. Conversely, one should then expect yields to go down (to reflect expectations of lower inflation?) as QE2 tapers off.

According to Morgan Stanley's David Greenlaw and absent the Fed as a marginal buyer the US Treasury will need, once again, to call upon an old faithful buyer.

Given that Treasury issuance is expected to continue at an extremely elevated clip for the foreseeable future, how will the market adjust to the loss of most Fed buying? In other words, who will be the marginal buyer of Treasuries going forward? Our analysis suggests that heavy buying by the largest foreign holders of Treasuries will be needed to avoid a back-up in yields.

Indeed, on this reading the end of QE2 looks very significant indeed.

I would re-emphasize here that despite Greenlaw's main argument that there is little scope for further purchases by domestic actors a steadily deteriorating macroeconomic landscape should be bullish for treasuries all things equal, but I concur that without the Fed the market may start to get a little more attached to the supply side story.

On balance it would then seem that the consensus remains weighed towards no QE3 either because it is not needed or because it does not work in the first place. I think it is very simple in the end though. If sideways movement gives way to a new downside in the market below key support levels it will be very easy for the Fed to argue for a new round of QE which I think they will deliver in due time.

---