QE and the Wealth Effect in the US

Events in Japan and Libya do not seem to have derailed the ongoing positive sentiment in the market, but it might just have alerted various Masters of the Universe that black holes (or was that swans?) are both invisible and unpredictable until they occur. It is precisely because of this that such events are important even if I think that hedging against so-called "tail risks" by buying specially tailored financial products is probably as effective as buying an extra swim suit in anticipation of the next tsunami.

On that note and if there ever was a clearly signalled change in the daily state of the market it is the end of the Fed's QE2 and thus the end of unconventional monetary measures by the Fed. It would then seem to be a simple exercise of discounting information which is already incorporated into current market prices, but it is anything but. This is due to two things in particular;

- While it is certain that QE2 will end, it is considerably more uncertain whether QE itself will end and it seems as if the market is implicitly expecting a continuation in the form of QE3. But it is not clear cut. The macro picture is brightening in the US and Fed officials are getting more hawkish and what was certain a few months ago, may not be so certain today. In addition, if the perception changes into an expectation of an end to QE the path and pace of the Fed's exit strategy is also uncertain.

- There is considerable uncertainty (and disagreement) as to the exact effect of QE in the first place and this shows itself on two fronts. One is the discussion of whether QE has been a success or not and the second is the more technical (yet equally important) question of through which channels QE can be shown to work (if at all). Krugman recently suggested the exactly the stock market effect which this post is based on.

In order to get to grips with this I thought it would be apt to center my analysis on the horse's own mouth as it were and specifically the idea that the Fed is targeting stock prices. Obviously, if asked directly Bernanke and his colleagues would certainly point out that it is not all about stock prices but a much more complex issue of affecting rates on all maturities of the yield curve as well as to repair the the monetary policy transmission mechanism as well as the monetary multiplier.

Yet, given chairman Bernanke's comments that the success of QE2 is linked to rising stock prices I thought it would be interesting to have a look at the macroeconomic effect of rising stock prices and thus the idea of the wealth effect. This is to say, what is the effect of rising stock prices on personal consumption expenditures and thus, in some sense, growth?

In summary, my analysis gives the following hints to the wealth effect in the US

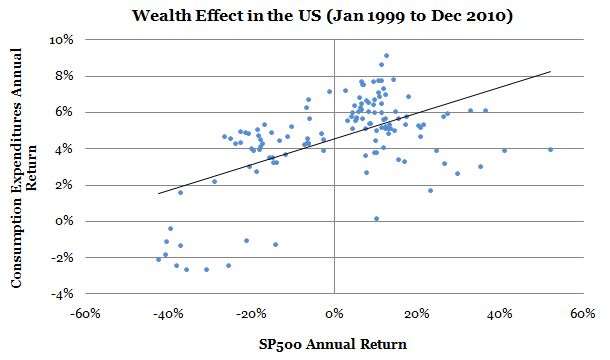

- The wealth effect from the stock market in the US is time variant but appear to be particularly strong in the period 1999 to 2010 which, in some sense, validates the Fed's focus on stock prices.

- The wealth effect also shows up in a negative relationship between changes in the SP500 and changes in the saving rate which suggest that rising asset prices may counteract deleveraging.

- The fiscal multiplier estimated here is also time variant and seems to change signs across periods.

- The marginal propensity to consume seems to have risen over time in the US.

Here, the two last bullet points are secondary to the main focus of this note but still worth thinking about.

(click on pictures for better viewing)*

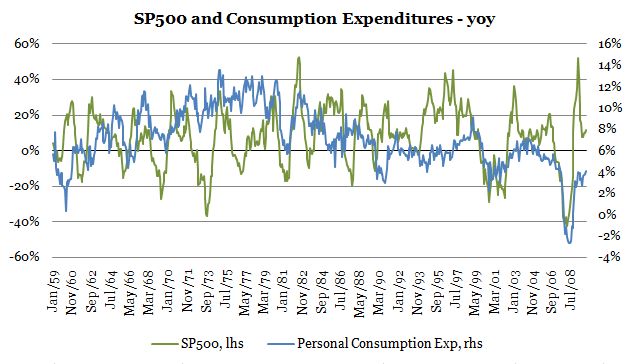

At a first glance, it is difficult to see any meaningful correlation between the two, but look closer at the period from 2007 and onwards (as well as in 2001) and you will see a closer semblance. But this may also be a case of the infamous spurious correlation as stock prices and consumption are strongly correlated around recessions and thus also in the rebound.

Surely, the linear fit depicted above for the full period is not statistically significant which suggests that measured over the grand sweep of time there is no meaningful correlation between changes in stock prices and changes in consumption expenditures. Importantly, this would also seem to invalidate the Fed's link between QE2 and rising stock prices since such a link is empirically dubious at best. Yet, as the graph from the period 1999 to 2010 shows the link may have strengthened.

To that end I have conducted a small study fitting a linear model with the annual change in consumption expenditures as dependent variable to the change in the SP500 as well as government transfers and real disposable income to control for the marginal propensity to consume and the fiscal multiplier. I use monthly values to get 612 observations in the full sample regression (1960 -2010). Crucially, I split up the dataset in three periods; 1960-1980, 1981-1998, and 1999-2010.

In the full period, the estimation gives an MPC of 0.41 [1], a multiplier from government transfer worth of 0.09 and from the SP500 equal to 0.027 (all significant at 1%). This implies that a 1% annual return in the SP500 yields an increase the annual change of consumption expenditures of 0.027%, but the results also indicate that the "fiscal multiplier" is about three times larger. So, not exactly convincing results to support QE as an attempt to boost consumption through the stock wealth effect.

Splitting the period as noted above [2] does seem to add value to the analysis. For the period 1960-1980 the simple OLS estimate yields nothing and not even the estimate for the MPC is significant [3]. In the period from 1981 to 1998 the MPC is estimated to be 0.48, the multiplier from government transfers at 0.14 and lastly for the SP500 at 0.014 although this estimate is only significant at 10%. The period from 1981 to 1998 thus return a strong fiscal multiplier (at least in terms of significance) while a weak, at best, multiplier from the SP500.

In the final period however, something interesting happens. The MPC increases to 0.58 which squares well with the declining saving rate in the same period. More interestlingly however, the estimate for the fiscal multiplier changes signs while remaining significant at 1%. The estimate suggests that a 1% increase in government transfers will yield a -0.36% decrease in consumption expenditures. Surely, proponents of Ricardian Equivalence would be interested in testing more thoroughly for the validity of this estimate. Meanwhile, the estimate for the wealth effect from stocks is estimated at 0.035 and significant at 1% (and thus quite close to the wealth effect estimated in the full period).

Finally, and focusing on the period 1999-2010, I also fitted a linear model with the savings rate as dependent variable. The rationale here would be that the wealth effect from the stock market should materialise in a negative relationship and thus that a rising stock market would counteract deleveraging. Not surprisingly the coefficients for both changes in income and changes in government transfer are positive which suggests that higher income and transfers from the government leads to higher savings (that Ricardian Equivalence again?). The coefficient estimated for the SP500 is negative and much higher than the wealth effect to consumption. All estimates are significant at 1%.

The What, Why and Where of QE

As my readers would no doubt remind I have added nothing to the debate of whether QE affects stock prices in the first place and then has an effect on the real economy through the wealth effect. I have taken this as given on particular notice of Bernanke's explicit comments on the success of QE2 in relation to a rising stock market.

As it turns out, the story is a bit more complicated than that.

Take Morgan Stanley's Gerald Minack for example who recently came out strongly against the notion of QE as a driver of risky assets which invariably leads to a much more bullish and broad based recovery discourse;

I am pushing back against the view that QE – particularly the large-scale asset purchases – directly drives risk assets. The reason I am skeptical is that no one has to my satisfaction explained how – sentiment aside – QE has had a material effect on the demand for, or funding of, risk assets. It’s not even straightforward to isolate the effect of QE on the assets that the Fed purchased.

(...)

As I see it, QE2 was a $600bn placebo. If enough investors think it was good for risk assets, then perhaps it was good for risk assets. Stopping the placebo may have an effect, but my sense is the macro will remain the key driver of risk assets.

The first part of Minack's objection to the QE-Risk Asset synthesis is important and I have also found it difficult to replicate the idea that QE directly drives risky assets . But the link need not be that specific for the end of QE to have an adverse effect of the growth narrative. I think the underlying reason as to why the market may now be driven by the improving macro picture is exactly because QE is seen as an integral part of that improvement. It then stands to reason that if and when QE ends (without extension) it will have an impact. Another point relates to the idea that the commitment itself to QE is paramount and thus that the largest effect of QE is back loaded around the announcement [4]. I think it is an accurate way to frame the effect of QE but this also implies that a second layer of expectations may take hold in the form of the expectation of the announcement. In reality, it is difficult to see how many of these "announcements" the market has discounted I think.

An altogether more heavy analysis recently came from CSLA's Russel Napier simply noting that investors ought to sell US equities on the failure of QE2. Napier particularly makes the point that QE2 has materially failed to induce banks to increase credit.

Broad money has contracted since the launch of QEII in November 2010 and this suggests that rising growth and inflation are not likely. QEII is boosting unused bank reserves, but banks continue to shrink credit and it is having no direct positive economic impact beyond depressing Treasury yields. Equity-market valuations are close to bubble levels and need the prospect of higher inflation and negative real rates to continue higher: but M3 is contracting.

(...)

The failure of QEII will undermine investor faith in a monetary solution. With equities near bubble valuations, based on cyclically adjusted PE, a failure to reflate risks major downside. The Fed will try again with a new package, but investors would do best by waiting to see how it plays out.

This analysis then suggests a much more imminent and substantial effect of the alleged failure of QE2 and thus also the effect of a non-committal to QE3. Clearly, we are now in the situation where this illusive concept of the monetary transmission mechanism becomes important.

Thus, has QE2 succeeded because it has helped equity prices to rally or has it been a failure because of its inability to induce more than an increase in excess reserves?

I won't pretent to give full answer on this (Napier's analysis is difficult to disagree with) and I would like instead to yield the floor to John P. Hussman who recently had a very well written and balanced column on the end of QE2;

My intent is not to argue strongly that the economy cannot continue to expand as fiscal and monetary stimulus comes off, but instead to at least ask why this should be expected as a foregone conclusion. On the basis of leading indices of economic activity, we observe more indications of economic slowing worldwide than we observe growth. Moreover, strong periods of employment growth have historically been preceded by high, not low, real interest rates. This is far from a perfect relationship, but it is clear that historically, high real interest rates are far more indicative of strong demand for credit, new investment, and new employment than low real interest rates are.

I would file this under "I'd wish I said that". The big question then remains as to what kind of momentum the economy and risky assets will retain once stimulus comes off.

To summarize, I have been critical of the Fed's decision to tie its policies so close to the movements of the stock market and I still am. The idea to implicitly target stock prices is the ultimate form of hubris that a central banker can commit since it plays into the notion that the central bank can consistently fine tune financial markets. It can't. However, my analysis above gives some support to the idea that QE works, and works well, through its effect on stock prices. At least, I would note that the extent to which e.g. Krugman is right the apparent change in the wealth effect over time gives some credence to Bernanke's comments in 60 minutes even if I don't agree with the Fed's strategy on this point.

---

* The data used for my estimations are monthly data from the St. Louis Fed's database.

[1] - Clearly this is below traditional Keynesian estimates but remember that we have monthly data in changes and thus likely to have stationary time series (i.e. we have detrended series!).To be rigorous one would obviously have to properly test the unit root properties of the series in question.

[2] - I am considering writing this up as a small paper trying to quantify the structural breaks in the data as well as to fit a non-linear model.

[3] - Which points to the notion developed exactly by researchers (Friedman for one) using data for that period that consumers spend out of permanent income and not current income.

[4] - I believe Goldman Sachs made a top notch study on this.