Checking up on the Consensus Trade

One of the main investment and trading themes crystallised during Q4-10 was the move out of emerging markets and into developed markets. As all themes, it started as a contrarian misfit moving against the truck loads of capital piling into emerging markets but has now reached its mature state flapping its wings as a beautiful butterfly and the main investment theme du jour. We know this because the Economist devoted a piece to it in their latest print edition;

(quote, the Economist)

One reason to look elsewhere is that Western economies’ prospects look sunnier than they did a few months ago. American consumer confidence has rebounded more quickly than expected, for instance. Much of the money that has come out of emerging economies has gone straight into developed markets, in what Michael Hartnett at Bank of America Merrill Lynch has dubbed the “Great Rotation”. Rich-world stockmarkets may also be the big beneficiaries of reallocation by fixed-income investors who believe that the bull run in bonds is over, says Nick Smithie of UBS.

The obvious question is whether it is too late to join the party now that the story has hit the mainstream press. The trend following crowd would doubtlessly argue for you to jump the bandwagon.

In so far as goes the idea that the relationship between emerging markets and developed markets should be enjoying an equal share of the excess liquidity sloshing around, there is certainly plenty of scope for further out performance of the developed markets. This notion is supported I think by the fact that the overall emerging market index has only recently started to correct downwards (in the aggregate). This is in contrast to the canary in the coal mine in the form of India whose equity markets have been resolutely hammered so far in 2011. This is perfectly predictable since India runs a current account deficit and is largely funded by short term maturity inflows.

I would even venture as far as to call it the revenge of text book economics as the current state of affairs fits very well into the (fairy)tale taught on international finance programs of the benefits of international diversification. A fully diversified international investor would thus currently be sporting a nice gain on any stock holdings in developed markets (in the US in particular). Indeed, if the main story of the post financial crisis world has been that of impaired monetary transmission mechanisms in the US and thus how Bernanke's free money flowed towards emerging markets, it seems as it has been temporarily restored.

Or has it?

It is precisely this meltup which has emerging market central banks scrambling to cool down their economies and which has currently set a vicious circle in motion for EM risky assets. Higher inflation in itself is detrimental to economic activity and as higher activity leads to higher interest rate/tightening expectations which again leads to lower economic activity. Within this circle the dilemma persists. How do you cool down your economy when raising interest rates runs the risk of attracting even more yield hungry capital? Turkey recently lowered interest rates and while everyone seems to be talking about the Indian central bank being behind the curve I think it is deliberately pursuing this strategy as it knows how raising interest rates may not be consistent with its objectives.

I for one was quite worried to hear Bernanke openly admit that the main criteria of success of QE2 is the fact that the stock market is going up. My view of the Fed policies is that they are trying to put weight against what they see as an inevitable and long process of deleveraging in the domestic economy and that this deleveraging is best dealt with in the face of rising risky assets (which is obviously de facto true in the US with a strong wealth effect from rising stock prices). I believe that the Fed is right to pursue extraordinary policies, but by marrying himself to the stock market Bernanke is playing a game he cannot win.

The main effect of QE2 was always to bid up commodities and risky assets across the board and together with a number of adverse supply shocks in the agricultural sector we are looking at a nasty meltup in 2011. I think that the current goldilocks recovery in the US supported by no imminent threat of interest rate hikes by the Fed (no matter the benevolence of the data!) is bullish for US stocks, but nothing goes up for ever and technically we have been on the brink of a correction for a long time.

If we manage to blow off some steam from the US stock markets, I think it will be a good idea to sling shot your way onto the developed market out performance theme, but for god's sake do not buy US beta for the long term at these levels!

TMM remind us that even with consensus trades, there is a limit to the degree of love and trend following.

As for DM Equities, we are just soooooo wanting them to fall over, having been on the bull bandwagon for so long, it's time to switch allegiance and play for a move down... How far? Not sure yet and we'll play that by ear, but new highs will have us out.

Perhaps spoken of one who would be able to take profit on a long DM position, but also an astute warning to those about to jump in the pool.

In this vein allow me to offer the contrarian perspective on the current consensus trade;

Look to build emerging market exposure in your long term investment portfolios

Chris Wood who pens the indispensable Greed and Fear for CLSA puts it very well;

With so much money invested in markets like India and Indonesia last year, there is clearly the potential for more selling on a flow of funds basis whatever the fundamentals. Still GREED & fear remains of the view that one of the most interesting opportunities provided by the present inflation scare will be for investors to buy the likes of India and Indonesia at significantly lower levels.

If 2011 turns out to be marred in a nasty meltup of headline inflation, emerging markets will suffer much more. Wood notes India and Indonesia where I have my eyes firmly fixed on the former for some stock pickings. But even by buying into beta at good levels, I think you can secure some nice future returns on that pension portfolio. Actually, this is a prime lesson in the difference between trading and investing for the average retail parasite.

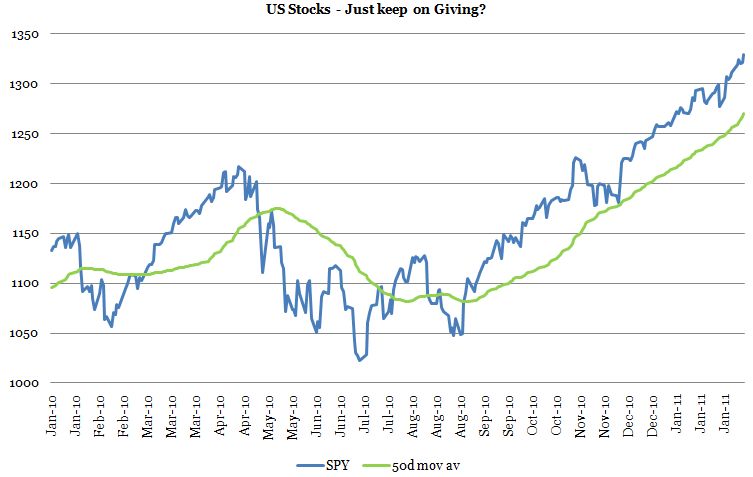

What happened last time we saw developed market out peformance?

Looking at the chart above the astute investor will immediately note that the last time we saw significant out performance of the developed market sector, it coincided with a sharp drop in global equity prices (you know, the crisis and all). Now things are obviously different you might plead. We are in a nascent recovery and global equity markets are powering ahead even as emerging markets struggle no doubt much to the pleasure of authors of finance text books.

However, it is quite easy to build the case for a very sinister hoax played on international investors piling into the broad based recovery story. Thus, I don't think that the global monetary tranmission mechanism has changed. Structurally, we still have to much capital chasing to little yield and while it should favor emerging markets in the long run it adds volatility their business cycle and thus the global business cycle too. The main worry at the moment in this respect is the prospects of a hard landing in China which would have strong global effects. In this sense, if the emerging markets experience a hard landing it stands to reason that it will be a global one too, de-coupling runs two ways!

This then becomes an argument for reducing the blind exposure to the QE2 punt and the goldilocks US recovery.

Remember the Fundamentals

Despite the current surge in headline inflation the main challenge for developed markets which remains fundamentally unsolved is how to generate growth while simultaneously consolidating public finances. The Eurozone periphery is merely a taste of fundamental problems to come. The recent fiscal monitor by the IMF should put a scare into even the most ardent bull;

Despite the improving global outlook, the pace of fiscal consolidation this year is slowing in some key countries. The United States and Japan are adopting new stimulus measures and delaying consolidation relative to the pace envisaged in the November 2010 Fiscal Monitor. The underlying fiscal outlook has also weakened in some emerging markets—among them are several that need to build larger fiscal buffers, particularly in the face of surging capital inflows, overheating, and possible contagion from advanced countries. By contrast, advanced economies in Europe are projected to continue tightening policies amid heightened market scrutiny in several countries. Altogether, sovereign risks remain elevated and in some cases have increased since November, underlining the need for more robust and specific medium-term consolidation plans.

I am not sure the IMF really knows what it is they are saying here, but go to the two charts in the blog post by Carlo Cottarelli and notice that advanced economies are to consolidate less than expected in 2011. Obviously, this is unsustainble but the flip side of this argument (and something I'd wish the wise people at the IMF would push stronger) is that national governments are waking up to the cruel reality that without fiscal stimuli there will be no growth. Indeed, some politicians will have to navigate an environment where the absense of continuing support by fiscal spending (financed by the central bank or domestic savings) is the only source of growth until some form of export apparatus might be put in place if at all. Allow me to repeat myself for the umpteenth time.

What happens once it dawns on investors that the trend growth rate in many OECD economies is negative absent fiscal deficits? Indeed, what happens when everyone realises that the only way to survive is to export and build a strong net foreign asset position?

I believe that this fact as it will reveal itself moving forward will have wide implications for sovereign debt and global growth dynamics. And while the time may not be now, it also implies a wholly different approach to the recent out performance of developed markets even if this particular theme, as a trade, may still have some time to run in 2011.