Divergence

I am a great believer in divergence when it comes to the talking about the economy and her markets because it allows you to take a slightly more nuanced perspective than the risk off/risk on debate that has dominated the discourse for the past two years now.

The Global Economy

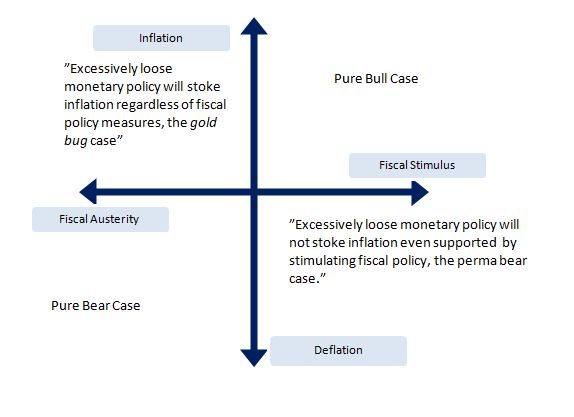

Still, there is much to suggest that when it comes to global economic discourse whatever your take on things is it follows an easily identifiable framework (click for better viewing).

It is my bet that whatever your position is on global growth, markets, the future of the Eurozone, the prospects of a bubble in China, inflation in India, the price of base commodities (etc etc) you will find yourself comfortably positioned somewhere in the matrix above. In fact, it is hard to form an opinion today on the global economy and its sub-components without taking a decisive stands along the spectrums above. Naturally though, there is more than meets the eye.

Note in particular that I take "excessively" loose monetary policy as given since here we find another case of divergence. Essentially, the debate is currently raging between those who advocate fiscal austerity as a precondition to securing future growth and those see it as a repetition of the same mistakes that were made in in 1937 as policy makers in the US assumed that the recovery was already a reality. Yet, when it comes to monetary policy it is taken as given that rates will stay near zero in the G3 for at least the next 8-12 months. Again, we have divergence here; divergence between policy positions and debates, but also divergence between global monetary policy regimes since you can just ask Reserve Bank of India Governor Duvvuri Subbarao what he thinks of loose monetary policy as he recently headed a 0.5% upward move in the base rate which widens the spread to the G3 even further.

Divergence here of course plays to the disadvantage of both monsieurs Trichet/Bernanke and Subbarao since the money created by the former won't stay to help their ailing economies but, in stead, race off to India (and elsewhere) fuelling an already raging inflation bonfire. Recently, the IMF downgraded its forecast for global growth (relative to pre-crisis levels) and thus in some sense lowered the bar for the natural speed limit of the global economy. It would however be too pessimistic to interpret this as secularly bad news since divergence will be the key word going forward on the macro level. Especially, the divergence between those economies with sufficient domestic demand capacity to reach "escape velocity" and those whose domestic economic momentum is essentially deflationary is a key theme.

To Pick or not to Pick

Another case of divergence which I recently picked up on is the growing discomfort among value investors that the gains from stock picking is being traded away. This is a long running theme on FT Alphaville and this week it is running two stories which push this point of view. The first is the coverage by Izabella of this piece in which Toronto-based money manager Friedberg Mercantile describes the pain of seeing its long time old and faithful market neutral strategy collapsing due to the correlation of everything. Of course this is not a cry-baby defence piece and it tracks its issues to a lack of dispersion between stocks due, in part, to the rise of exchange traded funds (ETFs) designed to mimic an index or specific asset class.

But this is not all and Ms Kaminska continues her coverage on this by pointing to a piece from Barclays Capital equity research people which lays out the same story. I especially like the point that while equity correlation remains a function of volatility the increasing run to index traded products increases the base level of correlation.

To summarize, in our opinion, while equity correlation continues to be highly dependent on volatility, the rise in indexation has led to a permanent increase in its “base” level. Thus while we do believe that the current high levels of realized and implied correlations are unsustainable, the eventual drop is not likely to be as high as some market participants might expect.

I think this is a very interesting point.

I do also find it almost ironic since one could arguably point to the fact that an increasing focus on buying the market (or a specific asset exposure/class) would mean that value investors got better prospects of carving out niches for them to excel in.

As for the divergence in all of this, you should by no means think that the value investor narrative is dead and buried. Today, Greg Donaldson (the director of Portfolio Strategy of Donaldson Capital Management) has penned a story over at Seeking Alpha in which he specifically suggests that retail investors go for single stocks and not "the economy".

What retail investors may be missing is that they are not investing in the economy. They are investing in companies. And, some - even many - companies can do quite well even during weak economies.

This point was recently given a run in the always excellent research from BCA (no link available) where they made a classic analysis of the SP500 sectors adjusting weightings based on valuation metrics and thus that positive returns were to be found in a market which traded sideways or even corrected downwards. Of course, they did talk about sectors but still the message was very much one of divergence based on fundamentals despite overall head winds to the economy. Similarly and despite the almost non-event of the recent Eurozone stress test one theme which emerged was indeed that investors could now discriminate between banks based on on their disclosure of sovereign debt holdings. Intuitively, this makes sense too I think, but if everything is correlated should you willingly allocate funds to such a strategy?

Where do you belong?

As ever, picking the right strategy or formulating your own and informed opinion on global economic and financial matters is just as much a question of where you don't fit in as where you fit in. Be it a question of the main fault lines of the global economy, the right between loose/tight monetary and fiscal policy or the right investment strategy divergence is the name of the game and choosing the right side of the fence is not only important for your own intellectual satisfaction, but also may be important for your portfolio.