Rebalancing in the Baltics - A Preliminary Assessment

"In my view … it is impossible to understand this crisis without reference to the global imbalances in trade and capital flows that began in the latter half of the 1990s." Bernanke (2009)

Executive Summary

- Compared with the average quarterly value of GDP in 2007-08, the first two quarters of 2009 are down in nominal terms to the tune of 15.9%, 15.4% and 10.5% in Lithuania, Estonia, and Latvia respectively.

- The average quarterly current account deficit of the Baltics from Q3 2008 to Q2 2009 was mill 500 Euros. This amount to just 18% of the average quarterly current account deficit two years prior to the crisis. Consequently, the Baltics have delevered to the tune of 80% over the course of less than 1 year.

- In the two first quarters of 2009 (relative to Q1-2006 to Q4-2008), imports have contracted 16%, 33% and 11.5% more than exports in Lithuania, Latvia and Estonia respectively.

- In Euro terms, the Baltics have lost external financing to the tune of bn 1.87 Euros in the first half of 2009 compared to the peak of the boom which amounts to 12.6% of the entire region's GDP in the same period.

The quote above from Fed chairman Bernanke is ripped from the introduction of a recent conference paper drafted by international economics icons Kenneth Rogoff and Maurice Obstfeld who suggest that the financial and economic crisis that is currently making its presence felt across the global economy, at least in part, has something to do with the notion of global current account imbalances. Now, and in all modesty, this is something I have argued extensively at this space and in this way I welcome the likes of Messieurs Rogoff and Obstfeld in the fold. I tend to go, of course, for the big prize in my stubborn persistence on the link between global ageing, global imbalances and thus by way of deduction the economic crisis as we have come to know it.

Now, I am not going to treat this link here but merely point to the rather obvious question at this point in time, in the form of whether in fact the crisis itself has been a catalyst of re-balancing? At a first glance this would clearly seem to be the case. In a crisis driven decisively by a violent process of deleveraging, those economies who had hitherto relied on borrowing have now been forced to scale back (and essentially correct either through a debasement of their currency, internal price correction, or a combination of these two) and the nations that had delivered the funding have likewise been forced to accept that their external surpluses have shrunk in a comparative manner.

So far so good then, but what happens when we have to get the patient out of intensive ward; who will run the deficits and surpluses and what size will the imbalances, if any, be. This is a difficult question to answer, but it appears that with the US economy now being effectively forced to correct its external imbalance (be it with Europe, China, Japan et al kicking and screaming or not), we have a situation with a lot of would be exporters and very little importers.

If this is the general set piece, it was with some interest that I read this VOX.eu piece by Mr. Richard Baldwin and Ms Daria Taglioni which dryly submits the thesis that although it may appear that rebalancing is occurring, this is only as a byproduct of the crisis. From ther horse's own mouth;

Global imbalances are shrinking at a fabulous rate. This column argues that these improvements are mostly illusory – the transitory side-effect of the greatest trade collapse the world has ever seen. A global recovery will almost surely return the US, Germany, China and others to their old paths.

Not exactly the prospect we were all hoping for, but in the main I agree with this point except of course the small and important qualifier that the US economy will have to deleverage and reduce the external (and indeed internal) borrowing. Whether Germany, Japan, China will also need to export ... well, this is ultimately a question of finding a customer.

Rebalancing the Baltics?

The obvious question to arise at this point is obviously what all this has to do with the Baltics? Well, in a direct sense not a whole lot since as the Economist so famously put it, the Baltics remain piqsqueaks and whether we observe current account positions, of either negative or positive pedigree, at some 20% of GDP it won't do much to affect the global imbalances. However, in the light of the idea of rebalancing on the back of the economic crisis and whether this is sustainable let alone feasible, the Baltics become very interesting not least since they have chosen (or have been led into) a process of rebalancing through internal price deflation (devaluation) as their currencies, for now, remain fixed to the Euro. In that vein, I thought it interesting to have a look at how the Baltics have faired so far with a specific focus on the external balance.

Beginning however with a general view of the correction so far the picture is definitely one of a hard landing on the back of the economic crisis.

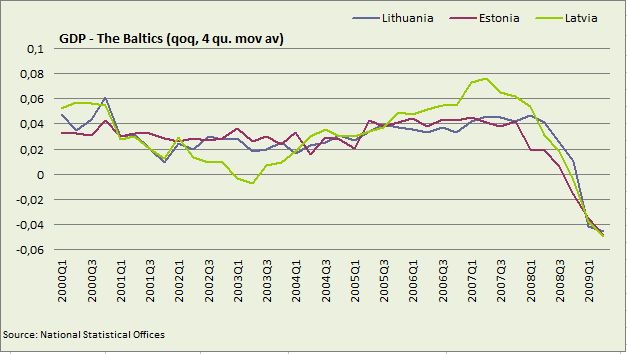

Most of the readers of this space will be well acquainted with travails of the Baltic economies (and in particular, the near collapse observed in Latvia earlier this year). In all three Baltic economies the Euro value of their GDP peaked in 2007-08 and has since fallen back dramatically. Compared with the average quarterly value of GDP in 2007-08, the first two quarters of 2009 are down in nominal terms to the tune of 15.9%, 15.4% and 10.5% in Lithuania, Estonia, and Latvia respectively. The Baltic economies have lost bn. 2.2 Euros worth of GDP in 2009 from the GDP output observed in 2007-08 which amounts to a loss of some 21% of the average value of the quarterly GDP output for all Baltic economies combined from 1999 to 2009. In short; these economies have taken some blow to the kidneys and even if we can safely say that the levels of nominal GDP observed in 2007-08 were unsustainable the way down is still rough, very rough.

Most of the readers of this space will be well acquainted with travails of the Baltic economies (and in particular, the near collapse observed in Latvia earlier this year). In all three Baltic economies the Euro value of their GDP peaked in 2007-08 and has since fallen back dramatically. Compared with the average quarterly value of GDP in 2007-08, the first two quarters of 2009 are down in nominal terms to the tune of 15.9%, 15.4% and 10.5% in Lithuania, Estonia, and Latvia respectively. The Baltic economies have lost bn. 2.2 Euros worth of GDP in 2009 from the GDP output observed in 2007-08 which amounts to a loss of some 21% of the average value of the quarterly GDP output for all Baltic economies combined from 1999 to 2009. In short; these economies have taken some blow to the kidneys and even if we can safely say that the levels of nominal GDP observed in 2007-08 were unsustainable the way down is still rough, very rough.

On the price front the correction has indeed begun and the graph above actually underestimates the current bout of price deflation as it smoothes away, as it were, the fact all three Baltic economies are in deflation on a m-o-m basis. Only Estonia registers deflation on my representation with Latvia basically hovering at the 0% line and Lithuania still producing inflation rates at some 2%.

Moving on to the external balance it is worthwhile splitting up the analysis by having a look at first the import/exports picture and then grinding down to the income level and finish off with a look at the financial accounts and thus the inflows used to finance the deficit (or how the surplus is invested abroad).

This is perhaps the best picture of the Baltic correction there is and nicely illustrates the point emphasised by Baldwin and Taglioni that the correction of imbalances, at this point in time, has been very much forced upon the deficit economies. Consider consequently the average quarterly current account deficit of the Baltics from Q3 2008 to Q2 2009 at mill 500 Euros; i.e. at the point when the crisis made its mark decisively.This amount to just 18% (!) of the average quarterly current account deficit two years prior to the crisis. This means that the Baltics have delevered to the tune of 80% relative to the level of the current account deficit observed up to the crisis. Again and with the benefit of hindsight, we know that these levels were unsustainable, but please do remember that it was only back in the H02 2008 that we were discussion whether the Baltics were going to have a hard or a soft landing. It is remarkable to note the example of Latvia here which has gone from a current account deficit of -17.6% of GDP in the period 2007-08 to a current account surplus of 14% of GDP (mill 681.3 Euros) in Q2 2009 due mainly to the fact that imports and GDP have plunged.

This point in particular is important to emphasize since the extent to which we are able to talk to about a sustainable (or benign if you will) process of rebalancing rather than one entirely driven by a sharp correction in internal demand and thus imports. The intuition tells us that Baltics are currently subject to the latter form of rebalancing and thus it remains to be seen whether there is a virtuous circle of increasing competitiveness and rising export shares (and values) on the back of the current vicious circle. But just how vicious is the current circle then?

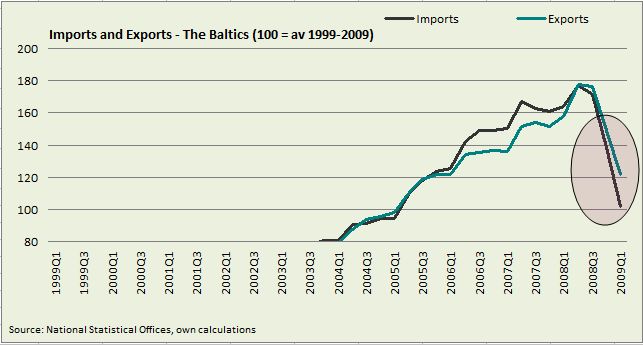

The graph to the right attempts to answer this question as it plots the equally weighted average of the evolution of exports and imports in the Baltics. The time series corresponds to the value of exports and imports in million of Euros of the three Baltic economies and is indexed with the average quarterly value between Q1-1999 and Q2-2009 of imports and exports as 100.

The graph easily shows how imports have contracted much more than exports and it is consequently here that we must look for the driver of rebalancing in the Baltics. If we take Q1-2006 to Q4-2008 as the peak of the boom (in terms of the external deficits), exports are down 10.8% in the first half of 2009 whereas imports are down a full 33.4% in the same period. This suggests that more than anything that rebalancing in the Baltics are currently driven by a sharp contraction of domestic demand. Splitting up the result on the three economies and looking exclusively at the second quarter of 2009, imports have contracted 16%, 33% and 11.5% more than exports in Lithuania, Latvia and Estonia respectively.

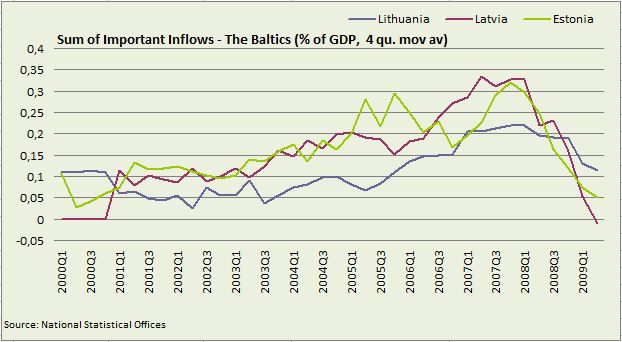

Another way to look at this is to approach the external deficit from the financing side and consequently have a look at the inflows used to finance the external deficits. In principle, you would normally and in the perfect world mainly look at portfolio and investment flows, but in the case of the Baltics we cannot neglect credit flows which, through all those Euro denominated loans supplied by Scandinavian banks, have been instrumental in driving the external deficits during the peak of the boom. If we begin with the inflows as a share of GDP we observe the drastic way in which the financing have been withdrawn in the context of the crisis.

Observe in particular the Latvian situation where an external surplus has been forced upon the economy, proxied here by "negative" inflows and thus outflows. In Lithuania, the total sum of important inflows had declined, as a share of GDP, to 60% in Q2-2009 relative to value recorded during the peak of the boom (Q1-2006 to Q4-2008). The corresponding figure for Estonia is 23% whereas for Estonia it has changed signs all together due to the fact that financing here has come to a complete standstill. In Euro terms, the Baltics have lost external financing to the tune of bn 1.87 Euros in the first half of 2009 compared to the peak of the boom which amounts to 12.6% of the entire region's GDP in the same period.

As noted extensively above, this process is natural since we can say with some confidence that whatever the level (and flow) of incoming investment and credit during the peak years it was not sustainable. However, when it happens with such force in the context of the global financial crisis and, moreover, in relation to fixed exchange regimes and thus internal devaluation the obvious question that begs is what the risk is of pushing these economies into a hole from which they cannot emerge. One particularly important point here is what kind of general (and domestic!) credit and financing environment we will see as the external funding is ground down and thus, in some sense, what kind of domestic environment the Baltics will have to stage a recovery in.

This last point is perhaps the most important underlying theme to think about when assessing the situation in the Baltics. We could almost say that the extent and pace to which the Baltics' growth path has crumbled is also the extent to which expectations of convergence, Euro membership, underlying growth potential etc have crumbled. Where we go from here is consequently anybody's guess. A lot of unresolved question still clouds the horizon not least the continuing unravelling in Latvia where the IMF has so stuck with the country despite the increasing dire outlook as long as the currency peg remains. What I can tell you however is that the Baltics are going to rebalance, but the key is the extent to which it happens so as to allow the Baltic economies to enter a virtuous circle somewhere down the road.

So far, a preliminary assessment suggests that while the Baltics are indeed rebalancing, they are only doing so because internal demand has caved in. We are yet to see whether the dose of internal devaluation/deflation will bring back competitiveness in due time to turn a vicious cycle into a virtuous one.